Why remittances need a crypto strategy

Sending money across borders remains inefficient for families relying on remittances. Traditional infrastructure imposes high fees and slow settlement times that erode the value of these critical transfers. A global crypto remittance strategy addresses these failures by leveraging technology to reduce costs and accelerate delivery.

The inefficiencies are stark. According to the World Bank, the global average cost of sending $200 remains above 6%, significantly higher than the UN Sustainable Development Goal target of 3%. Blockchain networks offer a way to bypass traditional correspondent banking chains, reducing fees to under 1% and cutting settlement times from days to minutes. This represents a fundamental shift in how value moves across borders.

Beyond cost, accessibility is a major failure point of traditional systems. Millions of people globally remain unbanked or underbanked, meaning they cannot easily receive or send money through conventional channels. Cryptocurrencies solve this by requiring only an internet connection and a digital wallet, not a formal bank account. As noted by Stripe, the technology reshaping cross-border payments is designed to address these exact accessibility challenges.

The urgency is compounded by regulatory changes. Starting January 1, 2026, a new 1% remittance transfer tax applies to remittances sent from the United States to foreign countries when paid via cash, money orders, or similar physical instruments. This policy, outlined by the IRS, targets traditional cash-based transfers, further incentivizing a move toward digital, traceable, and efficient crypto-based solutions.

Stablecoins anchor the global crypto remittance strategy

In a global crypto remittance strategy, stablecoins serve as the settlement layer because they bridge the gap between crypto’s speed and traditional finance’s need for predictability. Unlike volatile assets like Bitcoin or Ethereum, stablecoins maintain a peg to fiat currencies, typically the US dollar. This stability is non-negotiable for remittances, where the value of the transfer at the moment of sending must match the value received by the beneficiary. For migrant workers sending money home, a 5% swing in value during a three-day settlement window is unacceptable.

The technical infrastructure supporting stablecoins has matured significantly, enabling near-instant settlement across borders. Modern blockchain networks process transactions in seconds or minutes, compared to the three to five business days typical of traditional wire transfers. This speed is amplified by lower fees, which often undercut the 6-7% average cost of sending money globally reported by the World Bank. By bypassing correspondent banking networks, stablecoin transfers reduce friction and cost, making them ideal for high-frequency, low-margin remittance corridors.

| Feature | Traditional Wire | Stablecoin Transfer |

|---|---|---|

| Settlement Time | 3-5 business days | Seconds to minutes |

| Average Cost | 6-7% (World Bank) | Under 1% |

| Accessibility | Requires bank account | Internet + digital wallet |

Regulatory clarity is also shaping this landscape. New rules, such as the 1% remittance transfer tax proposed by the IRS for 2026, aim to standardize reporting but may inadvertently push some transactions toward crypto channels if compliance costs rise for traditional providers. Meanwhile, institutions like Stripe and Polygon are building enterprise-grade rails that integrate stablecoins into existing financial workflows, ensuring that businesses can adopt this technology without reinventing their compliance infrastructure. This convergence of speed, cost, and regulatory adaptation makes stablecoins the logical backbone of any forward-looking global remittance strategy.

Comparing blockchain networks for transfers

Choosing the right infrastructure for a global crypto remittance strategy in 2026 comes down to three metrics: fees, speed, and liquidity depth. While Bitcoin remains the anchor asset, its base layer is often too slow and expensive for frequent, lower-value transfers. Instead, most modern remittance flows rely on layer-2 solutions or alternative high-throughput chains to keep costs down and settlement times near-instant.

The table below compares the most common networks used for stablecoin remittances. These figures represent typical mainnet conditions for a standard $100 transfer.

| Network | Avg. Fee | Settlement Time | Liquidity Depth |

|---|---|---|---|

| Ethereum (L1) | $2.00 - $10.00+ | 12-15 minutes | Very High |

| Polygon | <$0.01 | 2-5 seconds | High |

| Solana | <$0.01 | 400 milliseconds | High |

| Bitcoin Lightning | Variable | Seconds | Medium |

Ethereum’s layer-1 network offers the deepest liquidity, making it the safest bet for moving large sums where counterparty risk is a concern. However, the gas fees can easily eat into smaller remittances. For everyday transfers, layer-2 solutions like Polygon or high-throughput chains like Solana provide a better user experience with negligible fees and near-instant finality.

Bitcoin Lightning presents a unique case. While it solves the speed and cost issues of the base layer, its liquidity is still fragmented compared to Ethereum-based stablecoins. If your recipients are in regions with limited crypto exchange access, sticking to widely supported chains like Polygon or Solana ensures they can cash out more easily. Always verify the receiving platform’s supported networks before initiating a transfer.

Navigating the 2026 Regulatory Landscape

The regulatory environment for crypto remittances is shifting from a gray area to a tightly controlled corridor. For any global crypto remittance strategy, compliance is no longer optional—it is the foundation. In 2026, the most significant change is the implementation of the US remittance transfer tax, which fundamentally alters the cost structure for cash-based cross-border payments.

This tax targets the informal and semi-formal channels that have long served unbanked populations. According to the IRS, this measure aims to bring transparency to cross-border flows that previously operated outside traditional banking oversight. For your strategy, this means that if your users rely on cash-to-crypto on-ramps, the cost of compliance and tax collection will be higher, but the net value proposition of crypto remains strong due to lower underlying transfer fees.

Beyond the US, global compliance requirements are converging. The Financial Action Task Force (FATF) guidelines on virtual assets are now being strictly enforced across major economies. This means your strategy must account for varying KYC (Know Your Customer) and AML (Anti-Money Laundering) standards depending on the destination country. A one-size-fits-all approach will fail; instead, you need a modular compliance layer that adapts to local regulations.

The World Bank continues to highlight that remittances are a critical lifeline for developing economies, often exceeding foreign direct investment. As governments clamp down on informal channels, the pressure is on crypto providers to offer seamless, compliant alternatives. The winners in 2026 will be those who can navigate this regulatory maze while keeping costs low and speed high.

For real-time market context, consider how regulatory news impacts crypto liquidity and exchange rates, which directly affect remittance costs.

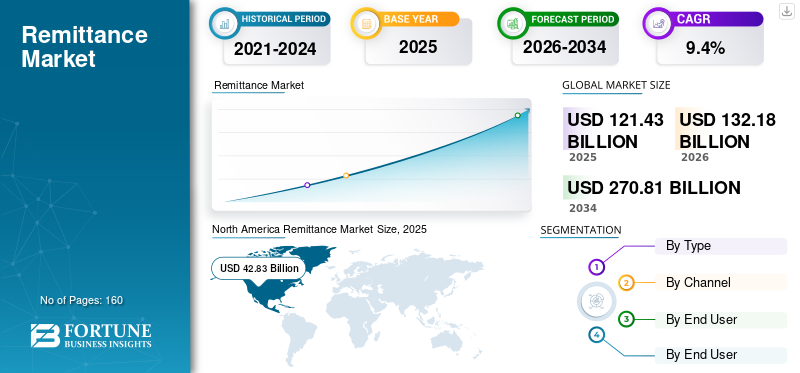

Top remittance corridors and market data

A global crypto remittance strategy must prioritize liquidity in the highest-volume corridors to minimize slippage and execution risk. India, Mexico, China, the Philippines, and Egypt consistently rank as the top five recipients of remittances, accounting for the vast majority of cross-border flows. According to the International Organization for Migration, money sent home by migrants has surpassed foreign direct investment in boosting the GDP of these developing nations.

The scale of this market is substantial. As shown in the chart below, the global remittance market continues to expand, driven by increasing migration and the need for efficient cross-border transfers.

Crypto’s primary advantage in these corridors is accessibility. Traditional remittances often require bank accounts, which many recipients in these regions lack. Cryptocurrencies only require internet access and a digital wallet, allowing senders and recipients to bypass traditional banking infrastructure entirely. This decentralization enables faster, cheaper transfers for the billions of people who rely on these funds for daily living expenses.

Frequently asked questions about crypto remittances

Who are the top recipients of global remittances?

India, Mexico, China, the Philippines, and Egypt consistently rank as the top five remittance recipient countries. According to the International Organization for Migration, money sent home by migrants abroad has surpassed foreign direct investment in boosting the GDP of developing nations. This massive flow of capital makes these regions prime targets for efficient, low-cost crypto remittance strategies.

What is the new 2026 remittance rule?

Beginning January 1, 2026, a 1% remittance transfer tax applies to remittances sent from the United States to foreign countries when the sender uses physical instruments like cash, money orders, or cashier's checks [IRS]. This regulation specifically targets traditional transfer providers. Cryptocurrency transactions, which are digital and decentralized, generally fall outside this specific tax framework, offering a potential compliance advantage for senders looking to minimize fees.

What problem does crypto solve for international transfers?

Cryptocurrencies address the accessibility gap that traditional banking leaves behind. Recipients do not need a formal bank account or access to traditional banking services to receive funds; they only require internet access and a digital wallet [Savannah Now]. This decentralization allows anyone, anywhere, to send and receive value without the friction of legacy financial infrastructure, making it a viable alternative for the unbanked population.

No comments yet. Be the first to share your thoughts!