Why remittance costs still matter

Cross-border payments remain a friction point in the global economy. Despite decades of digital innovation, the traditional banking system charges high fees and moves money slowly. For a global crypto remittance strategy, understanding this baseline problem is essential. If the status quo were efficient, there would be little incentive to build alternative rails.

The World Bank’s SDG target for remittance costs is 3%. In practice, global averages often hover between 6% and 7%, according to data from Stripe. This gap represents billions in lost value for migrant workers and their families. Georgetown Law notes that while cryptocurrencies offer a technical path to lower costs, they face their own hurdles, including financial complexity and knowledge barriers. However, the fundamental inefficiency of legacy systems remains the primary driver for adoption.

These costs are not just abstract percentages; they directly impact development in recipient countries. The United States, Saudi Arabia, and Switzerland remain the top remittance-sending nations, highlighting the scale of the market. A robust crypto strategy must address these high fees and slow settlement times to compete effectively with established money transfer operators.

Mapping the remittance infrastructure

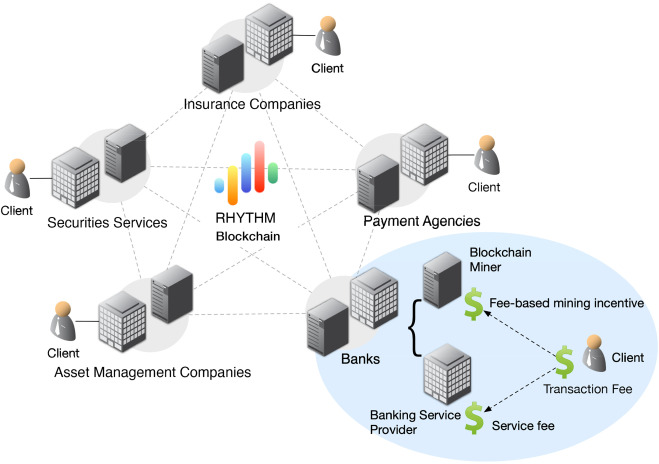

Building a global crypto remittance strategy requires more than just picking a coin; it demands a layered technical approach. You need settlement rails that move value instantly, networks that keep fees negligible, and reliable on/off ramps to bridge the gap between digital assets and local fiat currencies. Think of this infrastructure as the plumbing of your financial operation: if the pipes are leaky or clogged, the value never reaches the recipient.

Stablecoins have emerged as the preferred settlement layer for cross-border payments. Unlike volatile assets, stablecoins pegged to fiat currencies offer price stability while retaining the speed and transparency of blockchain technology. This makes them ideal for high-stakes financial decisions where predictability matters. As noted by industry analyses, stablecoins are lowering remittance costs and enabling faster settlement, gaining significant traction among banks and fintech platforms looking to modernize their cross-border capabilities.

Layer 2 (L2) networks solve the fee problem. By processing transactions off the main Ethereum chain before settling them back, L2s reduce gas fees by orders of magnitude. This is critical for remittances, where small transaction sizes can be eaten up by network costs. The combination of stablecoin settlement and L2 execution creates a cost structure that traditional banking rails struggle to match.

| Rail | Settlement | Avg. Cost | Regulatory Fit |

|---|---|---|---|

| SWIFT | 1-3 days | $15-$50+ | High (Legacy) |

| Stablecoins (L1) | 10-60 mins | $1-$10 | Medium (Evolving) |

| Stablecoins (L2) | Seconds | <$0.01 | Medium (Evolving) |

The final piece is the on/off ramp. This is where digital assets convert to local currency for the recipient. Providers like BVNK and Stripe are building the regulatory-compliant bridges necessary to move money in and out of the crypto ecosystem without triggering anti-money laundering (AML) flags. For a robust strategy, these ramps must be integrated seamlessly into the user experience, ensuring that the recipient gets fiat in their bank account or mobile wallet within minutes.

Compliance and risk layers

A global strategy must account for the fragmented regulatory landscape. While stablecoins offer efficiency, they operate in a gray area in many jurisdictions. Your infrastructure should prioritize providers that have navigated this complexity, offering built-in compliance checks and audit trails. This reduces the legal risk for both the sender and the receiver, ensuring that the remittance channel remains open and operational over the long term.

Tracking Global Flows and Institutional Adoption

The landscape of global crypto remittance strategy is shifting from niche experimentation to institutional infrastructure. As traditional finance players integrate blockchain rails, the focus has moved beyond simple cost savings to include speed, regulatory compliance, and liquidity management. Understanding these flows is essential for building a resilient strategy in 2026.

Top Corridors and Volume Trends

Remittance outflows remain concentrated in a few key economies, with the United States leading global outflows. According to data from the International Organization for Migration, the U.S. sent approximately $79.15 billion in 2022, followed by Saudi Arabia and Switzerland. Cryptocurrency is increasingly utilized in these high-volume corridors to bypass traditional banking delays, particularly where fiat liquidity is constrained or fees are prohibitive.

The shift toward stablecoins like USDT and USDC has driven significant volume growth in these corridors. These assets offer a stable bridge between fiat and crypto, reducing volatility risk for both senders and recipients. This stability has encouraged larger players, including fintechs and traditional remittance operators, to adopt blockchain-based settlement layers for cross-border payments.

The Institutional Shift

Institutional adoption is no longer a trend; it is the foundation of the modern remittance strategy. Major financial institutions are investing in blockchain infrastructure to streamline cross-border transactions, as highlighted by JPMorgan’s insights on fintech infrastructure. This shift is driven by the need for real-time settlement and reduced counterparty risk.

The integration of institutional-grade custody and compliance tools is enabling larger volumes to move through crypto rails. This institutionalization brings greater transparency and regulatory alignment, making crypto remittances a viable option for businesses and high-net-worth individuals alike. The result is a more robust, efficient, and scalable global payment network.

Market Data Overview

To monitor the health of the crypto remittance market, tracking stablecoin volume and price stability is critical. The chart below shows the recent performance of USDT/USDC, which serves as a proxy for remittance activity volume.

Selecting tools for cross-border efficiency

Building a global crypto remittance strategy isn't just about picking the cheapest coin; it's about assembling a stack that balances speed, cost, and security. You need infrastructure that handles the volatility and regulatory friction inherent in moving value across borders.

The core of your strategy relies on two types of tools: the settlement layer (blockchain) and the on/off-ramps (exchanges and payment processors). For high-volume transfers, stablecoins like USDC or USDT on low-fee networks (Solana, Polygon, or Layer 2s like Arbitrum) are the standard. They move fast and cost pennies compared to traditional SWIFT transfers. However, the real friction point is converting fiat to crypto and back again. This is where your choice of provider matters most.

For business-level efficiency, consider integrating with specialized remittance infrastructure like BVNK or Stripe. These platforms offer API-driven liquidity and compliance handling that generic exchanges often lack. They act as the bridge, ensuring your funds clear quickly without getting stuck in banking rails. For individual or smaller-scale remittances, non-custodial wallets with built-in swap features (like MetaMask or Rabby) offer more control but require you to manage your own security.

Essential Infrastructure Components

| Component | Role in Remittance | Key Consideration |

|---|---|---|

| Settlement Layer | Moves value instantly | Network fees and finality time |

| On/Off Ramp | Fiat-to-Crypto conversion | Regulatory compliance and liquidity |

| Self-Custody Wallet | Secure storage | Private key management and seed phrase safety |

Security: Hardware Wallets

If you are holding significant remittance funds, self-custody is non-negotiable. A hardware wallet keeps your private keys offline, protecting them from online hacks. For a global remittance strategy, you need devices that support multiple chains (Ethereum, Solana, etc.) and have a robust ecosystem of supported wallets.

As an Amazon Associate, we may earn from qualifying purchases.

Market Context

Understanding the underlying asset's performance is critical for timing your transfers. While stablecoins are pegged, the volatility of the base crypto (like Bitcoin or Ethereum) can impact liquidity and exchange rates during conversion.

Navigating regulatory compliance

Building a global crypto remittance strategy requires more than just finding the lowest fees; you must navigate a complex web of financial regulations. The high-stakes nature of cross-border payments means that non-compliance can freeze assets or trigger severe penalties. Your strategy must prioritize Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols to ensure legitimacy and trust.

Major jurisdictions are tightening their grip on digital asset transfers. For instance, the United States remains the top remittance-sending country, with outflows exceeding $79 billion in 2022, making it a critical focus for compliance frameworks IOM. Similarly, entities like Stripe and BVNK have had to adapt their services to meet evolving regulatory standards, ensuring that their platforms remain accessible while adhering to local laws.

Georgetown Law notes that cryptocurrencies are unlikely to provide a comprehensive solution to high remittance costs due to the inherent financial and knowledge-based barriers Georgetown Law. This highlights the need for a strategy that balances technological efficiency with rigorous regulatory adherence. You cannot simply bypass these requirements; you must integrate them into your operational model.

To stay informed on the market dynamics that influence these regulatory shifts, monitor key asset performance:

Frequently asked: what to check next

What problem do cryptocurrencies solve in international remittances?

Cryptocurrencies primarily address the high transaction costs associated with cross-border payments. Traditional banks and money transfer operators often levy significant fees, which can erode the value of funds sent to families abroad. By leveraging blockchain technology, crypto networks considerably lower these costs, allowing more of the sender’s money to reach the recipient. This efficiency is a core driver for adopting a global crypto remittance strategy, particularly for high-volume corridors like those from the United States to developing economies.

What are the top countries for remittance outflow?

The United States remains the dominant source of global remittances, with an outflow of approximately USD 79.15 billion in 2022. It is followed by Saudi Arabia (USD 39.35 billion), Switzerland (USD 31.91 billion), and Germany (USD 25.60 billion). Understanding these top outflow countries is critical for structuring a strategy, as liquidity and regulatory clarity often vary significantly between these major financial hubs and their corresponding receiving nations.

Can crypto fully replace traditional remittance services?

While blockchain offers speed and lower fees, it is unlikely to provide a comprehensive solution on its own. According to Georgetown Law, cryptocurrencies face hurdles related to financial complexity and volatility that traditional systems manage more predictably. A robust 2026 strategy typically integrates crypto for specific high-value or urgent transfers while maintaining fiat rails for broader stability, rather than attempting a complete replacement of existing infrastructure.

No comments yet. Be the first to share your thoughts!