Why traditional rails struggle with remittances

Sending money across borders has long been a friction-heavy process. For millions of workers supporting families abroad, the traditional banking system often feels less like a service and more like a tax on displacement. The core issue isn't just inconvenience; it's the structural inefficiency of legacy infrastructure that wasn't built for the speed or volume of modern global migration.

The cost barrier is significant. According to World Bank data, the average cost of sending remittances globally sits at 6.3%. While this percentage might seem small, it translates to billions of dollars lost annually for migrant workers who are already operating on thin margins. This fee structure includes not just explicit bank charges, but also the hidden cost of unfavorable exchange rates applied during the conversion process.

Settlement times compound the financial pain. A traditional wire transfer can take three to five business days to clear, depending on the currencies involved and the number of intermediary banks. In a volatile economic environment, that delay isn't just an administrative hurdle; it represents real risk. Prices can shift, and urgent needs can go unmet while funds sit in transit.

As international transfers are projected to grow by five percent annually through 2027, driven by previously unbanked populations entering the formal economy, the strain on these legacy systems will only intensify. The current model simply cannot scale efficiently to meet this demand without passing more costs onto the consumer.

Comparing blockchain protocols for cross-border value

Choosing the right rail depends on whether you prioritize speed, cost, or stability. The current infrastructure landscape offers distinct trade-offs between Layer 1 blockchains, Layer 2 networks, and stablecoin transfers. Understanding these differences helps businesses and individuals select the most efficient path for their specific transaction needs.

Bitcoin remains the most established network but faces scalability challenges for small, frequent remittances. Ethereum Layer 2 solutions offer faster settlement and lower fees by processing transactions off the main chain. Stablecoins, particularly USDT and USDC, provide price stability similar to traditional fiat currencies while leveraging blockchain efficiency.

The following comparison highlights the key operational metrics for each protocol type. These figures represent typical network conditions and can vary based on network congestion and gas fees.

| Protocol | Avg. Fee | Settlement | Volatility Risk |

|---|---|---|---|

| Bitcoin L1 | $2–$15 | 10–60 mins | High |

| Ethereum L2 | $0.01–$0.50 | Seconds–Minutes | High |

| USDT/USDC | $0.01–$1.00 | Seconds–Minutes | Low |

Each protocol serves different use cases. Bitcoin L1 is suitable for large, infrequent transfers where network security is paramount. Layer 2 solutions work well for frequent, smaller transactions requiring quick confirmation. Stablecoins are ideal for businesses needing predictable exchange rates without exposure to crypto market swings.

The scale of the global remittance market

The global cross-border payments market is not just growing; it is expanding at a scale that traditional banking infrastructure struggles to match. According to data from FXC Intelligence, cited by PitchBook, the total value of cross-border payments is projected to reach $290 trillion by 2030. This massive figure underscores why crypto remittance strategy is no longer a niche experiment but a critical component of modern financial infrastructure.

The growth is driven by both volume and accessibility. International transfers are expected to increase by five percent annually until 2027, fueled in part by previously unbanked populations gaining access to digital financial tools. As more people enter the formal economy, the demand for faster, cheaper, and more transparent transfer methods intensifies. Cryptocurrencies offer a solution that bypasses the legacy correspondent banking network, reducing friction and cost for these high-volume flows.

To understand the market context, it helps to look at the underlying asset performance that enables these transactions. The volatility and liquidity of major crypto assets directly impact the efficiency of remittance corridors.

This market trajectory validates the strategic importance of integrating crypto rails into broader remittance operations. For investors and financial institutions, the data points to a sector that is maturing rapidly, with clear demand signals from both institutional players and individual users in emerging markets.

Essential Tools for Executing Remittances

Executing a global crypto remittance strategy requires a stack of specialized tools. You need reliable software to manage digital assets and secure hardware to protect them. The right combination of exchanges, wallets, and payment rails determines whether your transfers are fast, cheap, and safe.

Digital Wallets and Exchanges

Software wallets act as the primary interface for sending and receiving funds. They connect to the blockchain, allowing you to manage stablecoins or other assets directly. For remittances, non-custodial wallets like MetaMask or Trust Wallet offer control without intermediaries, while custodial wallets provided by exchanges simplify the process for beginners.

Exchanges serve as the bridge between fiat currency and crypto. Platforms like Coinbase or Kraken allow you to convert local currency into stablecoins, which are then sent to the recipient. According to Stripe, these global and regional exchanges are essential for converting local currency to stablecoins and sending them to a recipient's wallet Stripe. This conversion step is often the most critical for users unfamiliar with crypto markets.

Hardware Wallets for Security

For significant amounts, hardware wallets are non-negotiable. Devices like Ledger and Trezor store private keys offline, protecting them from online hacks. They provide a physical confirmation step for every transaction, adding a layer of security that software alone cannot match.

As an Amazon Associate, we may earn from qualifying purchases.

Payment Rails and Networks

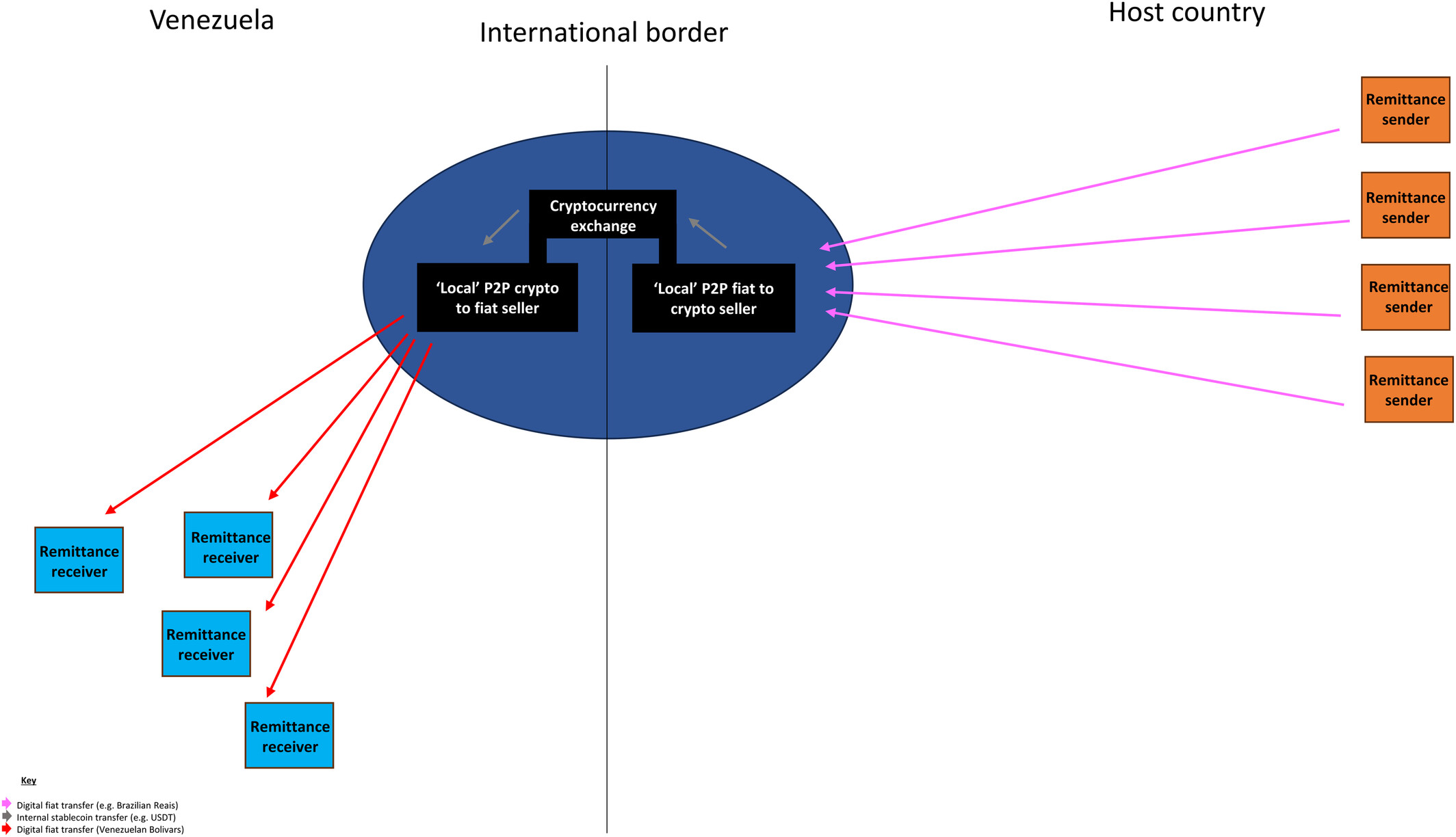

The choice of blockchain network impacts speed and cost. Ethereum is widely supported but can be expensive during high traffic. Solana and Stellar offer lower fees and faster settlement times, making them attractive for smaller, frequent remittances. Some exchanges now support direct fiat-to-fiat corridors using crypto as the backend rail, hiding the complexity from the user.

Live Market Data

Monitoring market conditions helps you time your conversions for the best rates. Use live widgets to track the assets you plan to send or receive.

Regulatory compliance and risk management

Use this section to make the Global Crypto Remittance Strategy decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Checklist for launching your remittance strategy

Launching a crypto remittance strategy requires more than just picking a blockchain; it demands a rigorous validation of compliance, infrastructure, and user experience. Before committing capital or routing volume, run through these five steps to ensure your operation is secure, scalable, and legally sound.

Start by mapping the legal requirements in both your origin and destination jurisdictions. Consult official regulatory bodies, such as the Financial Action Task Force (FATF) guidelines, to ensure your model meets anti-money laundering (AML) and know-your-customer (KYC) standards. Non-compliance is the fastest way to shut down a remittance operation.

Choose a network that balances speed, cost, and liquidity. For high-volume, low-margin transfers, stablecoins on established chains like Ethereum or Solana often provide the best infrastructure. Evaluate the gas fees and finality times, ensuring they align with your target customer’s expectations for instant, low-cost transfers.

Your strategy is only as good as your on-ramp and off-ramp liquidity. Vet your banking partners and exchange relationships to ensure they can handle the volume you plan to route. Secure commitments for fiat-to-crypto conversion and crypto-to-fiat payout, minimizing the risk of settlement failures during peak hours.

Never launch without a pilot phase. Run small, real-money transfers through your entire flow, from origin to destination. This tests the actual user experience, including wallet connectivity, transaction confirmation times, and the reliability of your payout partners. Identify friction points before they affect your reputation.

Implement institutional-grade custody solutions for any assets you hold. Use multi-signature wallets and hardware security modules to protect your operational funds. Ensure your key management system is audited and that you have a clear disaster recovery plan in case of security breaches or system failures.

By following this checklist, you build a foundation that is resilient to market fluctuations and regulatory scrutiny. This structured approach minimizes risk while maximizing the efficiency of your cross-border payment infrastructure.

No comments yet. Be the first to share your thoughts!